Applied Econometrics

(52 Einträge)

Lecture Applied Econometrics, 1. Lesson

| Title: | Lecture Applied Econometrics, 1. Lesson |

| Description: | Vorlesung im SoSe 2020; Montag, 20. April 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-04-20 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, |

| Identifier: | UT_20200420_001_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 2. Lesson

| Title: | Lecture Applied Econometrics, 2. Lesson |

| Description: | Vorlesung im SoSe 2020; Montag, 20. April 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-04-20 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, |

| Identifier: | UT_20200420_002_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 3. Lesson

| Title: | Lecture Applied Econometrics, 3. Lesson |

| Description: | Vorlesung im SoSe 2020; Dienstag, 21. April 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-04-21 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Applied Econometrics Study, Boon, Burden, Sovereign risk, Causality, Endogeneity, Reverse causality, |

| Identifier: | UT_20200421_001_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 4. Lesson

| Title: | Lecture Applied Econometrics, 4. Lesson |

| Description: | Vorlesung im SoSe 2020; Dienstag, 21. April 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-04-21 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Applied Econometrics Study, Boon, Burden, Sovereign risk, Empirical Analysis, |

| Identifier: | UT_20200421_002_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 5. Lesson

| Title: | Lecture Applied Econometrics, 5. Lesson |

| Description: | Vorlesung im SoSe 2020; Montag, 27. April 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-04-27 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Justification for (linear) regression, Structural model, |

| Identifier: | UT_20200427_001_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 6. Lesson

| Title: | Lecture Applied Econometrics, 6. Lesson |

| Description: | Vorlesung im SoSe 2020; Montag, 27. April 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-04-27 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Justification for (linear) regression, Structural model, Glosten-Harris model, |

| Identifier: | UT_20200427_002_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 7. Lesson

| Title: | Lecture Applied Econometrics, 7. Lesson |

| Description: | Vorlesung im SoSe 2020; Dienstag, 28. April 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-04-28 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Justification for (linear) regression, Structural model, Glosten-Harris model, Market Maker, Transaction price, Human Capital theory, |

| Identifier: | UT_20200428_001_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 8. Lesson

| Title: | Lecture Applied Econometrics, 8. Lesson |

| Description: | Vorlesung im SoSe 2020; Dienstag, 28. April 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-04-28 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Justification for (linear) regression, Structural model, Human Capital theory, Mincer equation, Linear factor asset pricing models, CAPM, Fama-French model, |

| Identifier: | UT_20200428_002_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 9. Lesson

| Title: | Lecture Applied Econometrics, 9. Lesson |

| Description: | Vorlesung im SoSe 2020; Montag, 04. Mai 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-05-04 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Easy Pieces, Linear Regression, |

| Identifier: | UT_20200504_001_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 10. Lesson

| Title: | Lecture Applied Econometrics, 10. Lesson |

| Description: | Vorlesung im SoSe 2020; Montag, 04. Mai 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-05-04 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Linear Regression, Classic Approach, Population Regression, |

| Identifier: | UT_20200504_002_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 11. Lesson

| Title: | Lecture Applied Econometrics, 11. Lesson |

| Description: | Vorlesung im SoSe 2020; Dienstag, 05. Mai 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-05-05 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Population Regression, Population regression coefficients, |

| Identifier: | UT_20200505_001_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 12. Lesson

| Title: | Lecture Applied Econometrics, 12. Lesson |

| Description: | Vorlesung im SoSe 2020; Dienstag, 05. Mai 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-05-05 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Linear Regression, Population Regression, Regression anatomy formula, |

| Identifier: | UT_20200505_002_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 13. Lesson

| Title: | Lecture Applied Econometrics, 13. Lesson |

| Description: | Vorlesung im SoSe 2020; Montag, 11. Mai 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-05-11 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Population Regression, Theory, Statistic, Linear Conditional Expectation Function (CEF), Linear Regression, |

| Identifier: | UT_20200511_001_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 14. Lesson

| Title: | Lecture Applied Econometrics, 14. Lesson |

| Description: | Vorlesung im SoSe 2020; Montag, 11. Mai 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-05-11 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Law of Total Expectation (LTE), |

| Identifier: | UT_20200511_002_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

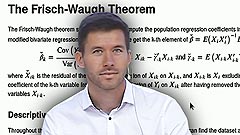

Lecture Applied Econometrics, 15. Lesson

| Title: | Lecture Applied Econometrics, 15. Lesson |

| Description: | Vorlesung im SoSe 2020; Dienstag, 12. Mai 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-05-12 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Frisch-Waugh Theorem, Proof, |

| Identifier: | UT_20200512_001_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 16. Lesson

| Title: | Lecture Applied Econometrics, 16. Lesson |

| Description: | Vorlesung im SoSe 2020; Dienstag, 12. Mai 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-05-12 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Frisch-Waugh Theorem, Constantin Hanenberg, Descriptive Statistics, |

| Identifier: | UT_20200512_002_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 17. Lesson

| Title: | Lecture Applied Econometrics, 17. Lesson |

| Description: | Vorlesung im SoSe 2020; Montag, 18. Mai 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-05-18 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Motivations for linear CEF, Double Expectation Theorem (DET), Generalized DET, Linearity of Conditional Expectations, |

| Identifier: | UT_20200518_001_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 18. Lesson

| Title: | Lecture Applied Econometrics, 18. Lesson |

| Description: | Vorlesung im SoSe 2020; Montag, 18. Mai 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-05-18 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Law of Iterated Expectation (LIE), Justification, Conditional Expectation Function (CEF), |

| Identifier: | UT_20200518_002_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 19. Lesson

| Title: | Lecture Applied Econometrics, 19. Lesson |

| Description: | Vorlesung im SoSe 2020; Dienstag, 19. Mai 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-05-19 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Justification, Linear Conditional Expectation Function, Easy Pieces, Multivariate Normal Distribution, |

| Identifier: | UT_20200519_001_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 20. Lesson

| Title: | Lecture Applied Econometrics, 20. Lesson |

| Description: | Vorlesung im SoSe 2020; Dienstag, 19. Mai 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-05-19 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Multivariate Normal Distribution, Saturated Regression, Justification, Best Approximation to nonlin. CEF, Optimal Prediction, |

| Identifier: | UT_20200519_002_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 21. Lesson

| Title: | Lecture Applied Econometrics, 21. Lesson |

| Description: | Vorlesung im SoSe 2020; Montag, 25. Mai 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-05-25 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, |

| Identifier: | UT_20200525_001_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 22. Lesson

| Title: | Lecture Applied Econometrics, 22. Lesson |

| Description: | Vorlesung im SoSe 2020; Montag, 25. Mai 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-05-25 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Rubin Causal Model, |

| Identifier: | UT_20200525_002_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 23. Lesson

| Title: | Lecture Applied Econometrics, 23. Lesson |

| Description: | Vorlesung im SoSe 2020; Dienstag, 26. Mai 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-05-26 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Justification, (Rubin's) causal model, Conditional Independence Assumption (CIA), Selection Bias, Matching Estimator, |

| Identifier: | UT_20200526_001_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 24. Lesson

| Title: | Lecture Applied Econometrics, 24. Lesson |

| Description: | Vorlesung im SoSe 2020; Dienstag, 26. Mai 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-05-26 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, |

| Identifier: | UT_20200526_002_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 25. Lesson

| Title: | Lecture Applied Econometrics, 25. Lesson |

| Description: | Vorlesung im SoSe 2020; Montag, 08. Juni 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-06-08 |

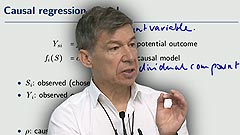

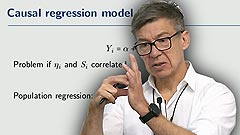

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Causal regression model, Long regression, Short regression, |

| Identifier: | UT_20200608_001_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 26. Lesson

| Title: | Lecture Applied Econometrics, 26. Lesson |

| Description: | Vorlesung im SoSe 2020; Montag, 08. Juni 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-06-08 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Difference-in-Difference Method, Parameter Estimation, |

| Identifier: | UT_20200608_002_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 27. Lesson

| Title: | Lecture Applied Econometrics, 27. Lesson |

| Description: | Vorlesung im SoSe 2020; Dienstag, 09. Juni 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-06-09 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Parameter Estimation, Hayashi, |

| Identifier: | UT_20200609_001_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 28. Lesson

| Title: | Lecture Applied Econometrics, 28. Lesson |

| Description: | Vorlesung im SoSe 2020; Dienstag, 09. Juni 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-06-09 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Parameter Estimation, Hayashi, |

| Identifier: | UT_20200609_002_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 29. Lesson

| Title: | Lecture Applied Econometrics, 29. Lesson |

| Description: | Vorlesung im SoSe 2020; Montag, 15. Juni 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-06-15 |

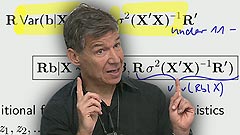

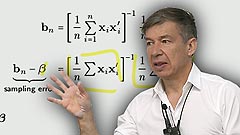

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Finite sample properties of OLS, OLS estimator, Sampling error, Unbiasedness, |

| Identifier: | UT_20200615_001_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 30. Lesson

| Title: | Lecture Applied Econometrics, 30. Lesson |

| Description: | Vorlesung im SoSe 2020; Montag, 15. Juni 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-06-15 |

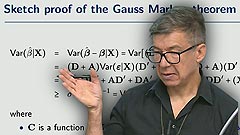

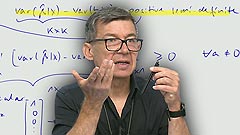

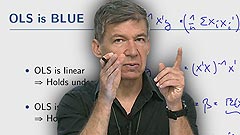

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Finite sample properties of OLS, Gauss Markov theorem, |

| Identifier: | UT_20200615_002_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 31. Lesson

| Title: | Lecture Applied Econometrics, 31. Lesson |

| Description: | Vorlesung im SoSe 2020; Dienstag, 16. Juni 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-06-16 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Q4R Fifth Week, Alina Schmidt, Omitted Variable Bias Formula, |

| Identifier: | UT_20200616_001_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 32. Lesson

| Title: | Lecture Applied Econometrics, 32. Lesson |

| Description: | Vorlesung im SoSe 2020; Dienstag, 16. Juni 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-06-16 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Constantin Hanenberg, Matching, |

| Identifier: | UT_20200616_002_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 33. Lesson

| Title: | Lecture Applied Econometrics, 33. Lesson |

| Description: | Vorlesung im SoSe 2020; Montag, 22. Juni 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-06-22 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, OLS, Hypothesis Testing under Normality, t-Test, Nuisance parameter, |

| Identifier: | UT_20200622_001_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 34. Lesson

| Title: | Lecture Applied Econometrics, 34. Lesson |

| Description: | Vorlesung im SoSe 2020; Montag, 22. Juni 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-06-22 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Hypothesis Testing under Normality, Confidence interval, F-Test, |

| Identifier: | UT_20200622_002_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 35. Lesson

| Title: | Lecture Applied Econometrics, 35. Lesson |

| Description: | Vorlesung im SoSe 2020; Dienstag, 23. Juni 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-06-23 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Hypothesis Testing under Normality, Waldtest, |

| Identifier: | UT_20200623_001_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 36. Lesson

| Title: | Lecture Applied Econometrics, 36. Lesson |

| Description: | Vorlesung im SoSe 2020; Dienstag, 23. Juni 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-06-23 |

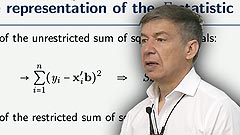

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Goodness-of-fit measures, Coefficient of determination, Large Sample Theory, OLS, |

| Identifier: | UT_20200623_002_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 37. Lesson

| Title: | Lecture Applied Econometrics, 37. Lesson |

| Description: | Vorlesung im SoSe 2020; Montag, 29. Juni 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-06-29 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Large Sample Theory, OLS, Modes of stochastic convergence, Law of Large Numbers (LLN), Khinchin's Weak Law of Large Numbers (WLLN), |

| Identifier: | UT_20200629_001_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 38. Lesson

| Title: | Lecture Applied Econometrics, 38. Lesson |

| Description: | Vorlesung im SoSe 2020; Montag, 29. Juni 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-06-29 |

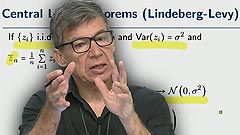

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Large Sample Theory, OLS, Law of Large Numbers (LLN), Khinchin's Weak Law of Large Numbers (WLLN), WLLN extensions, Central Limit Theorems, Useful lemmas, Continuous Mapping Theorem (CMT), |

| Identifier: | UT_20200629_002_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 39. Lesson

| Title: | Lecture Applied Econometrics, 39. Lesson |

| Description: | Vorlesung im SoSe 2020; Dienstag, 30. Juni 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-06-30 |

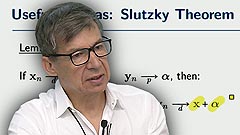

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Large Sample Theory, OLS, Useful lemmas, Continuous Mapping Theorem (CMT), Slutzky Theorem, Large sample assumptions for OLS, Large sample distribution of OLS estimator, |

| Identifier: | UT_20200630_001_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 40. Lesson

| Title: | Lecture Applied Econometrics, 40. Lesson |

| Description: | Vorlesung im SoSe 2020; Dienstag, 30. Juni 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-06-30 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Large Sample Theory, OLS, |

| Identifier: | UT_20200630_002_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 41. Lesson

| Title: | Lecture Applied Econometrics, 41. Lesson |

| Description: | Vorlesung im SoSe 2020; Montag, 06. Juli 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-07-06 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Large Sample Theory, OLS, White standard errors, Reduction to finite sample results, |

| Identifier: | UT_20200706_001_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 42. Lesson

| Title: | Lecture Applied Econometrics, 42. Lesson |

| Description: | Vorlesung im SoSe 2020; Montag, 06. Juli 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-07-06 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Time Series Basics, Stationary, Ergodicity, Time series dependence, Strict stationarity, |

| Identifier: | UT_20200706_002_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 43. Lesson

| Title: | Lecture Applied Econometrics, 43. Lesson |

| Description: | Vorlesung im SoSe 2020; Dienstag, 07. Juli 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-07-07 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Time Series Basics, Stationary, Ergodicity, |

| Identifier: | UT_20200707_001_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 44. Lesson

| Title: | Lecture Applied Econometrics, 44. Lesson |

| Description: | Vorlesung im SoSe 2020; Dienstag, 07. Juli 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-07-07 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, |

| Identifier: | UT_20200707_002_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 45. Lesson

| Title: | Lecture Applied Econometrics, 45. Lesson |

| Description: | Vorlesung im SoSe 2020; Montag, 13. Juli 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-07-13 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Multicollinearity, Endogeneity, |

| Identifier: | UT_20200713_001_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 46. Lesson

| Title: | Lecture Applied Econometrics, 46. Lesson |

| Description: | Vorlesung im SoSe 2020; Montag, 13. Juli 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-07-13 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Endogeneity, Reduced form, |

| Identifier: | UT_20200713_002_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 47. Lesson

| Title: | Lecture Applied Econometrics, 47. Lesson |

| Description: | Vorlesung im SoSe 2020; Dienstag, 14. Juli 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-07-14 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Endogeneity, Parameters of interest, Supply and demand model, Extended market model, |

| Identifier: | UT_20200714_001_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 48. Lesson

| Title: | Lecture Applied Econometrics, 48. Lesson |

| Description: | Vorlesung im SoSe 2020; Dienstag, 14. Juli 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-07-14 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Endogeneity, Simultaneity, Errors in Variables, |

| Identifier: | UT_20200714_002_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 49. Lesson

| Title: | Lecture Applied Econometrics, 49. Lesson |

| Description: | Vorlesung im SoSe 2020; Montag, 20. Juli 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-07-20 |

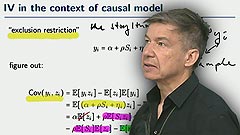

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Instrumental Variables (IV), Market model, Haavelmo, Errors in variable, |

| Identifier: | UT_20200720_001_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 50. Lesson

| Title: | Lecture Applied Econometrics, 50. Lesson |

| Description: | Vorlesung im SoSe 2020; Montag, 20. Juli 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-07-20 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Instrumental Variables (IV), Sampling error, Asymptotic Variance-Covariance Matrix, |

| Identifier: | UT_20200720_002_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 51. Lesson

| Title: | Lecture Applied Econometrics, 51. Lesson |

| Description: | Vorlesung im SoSe 2020; Dienstag, 21. Juli 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-07-21 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Causal regression with covariates, |

| Identifier: | UT_20200721_001_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |

Lecture Applied Econometrics, 52. Lesson

| Title: | Lecture Applied Econometrics, 52. Lesson |

| Description: | Vorlesung im SoSe 2020; Dienstag, 21. Juli 2020 |

| Creator: | Joachim Grammig (author) |

| Contributor: | ZDV Universität Tübingen (producer) |

| Publisher: | ZDV Universität Tübingen |

| Date Created: | 2020-07-21 |

| Subjects: | Wirtschaftswissenschaft, Applied Econometrics, Lecture, Causal model with covariates, Indirect least Squares (ILS), 2 stage least Squares (2SLS), |

| Identifier: | UT_20200721_002_appecono_0001 |

| Rights: | Rechtshinweise |

| Abstracts: | Students understand and apply important methods of applied econometrics. They reflect the assumptions and the intuition behind the different methods. The students perform econometric estimations and tests using econometric software and interpret the results in as scientifically correct way. The module discusses econometric models and estimation techniques. Topics presented include: 1. Regression analysis 2. Estimation and inference 3. Data and specification issues 4. Use of cross-sectional, time series and panel data 5. Sample selection corrections 6. Simultaneous equation models 7. Endogeneity: sources and solutions 8. Instrumental variables estimation and two-stage least squares |